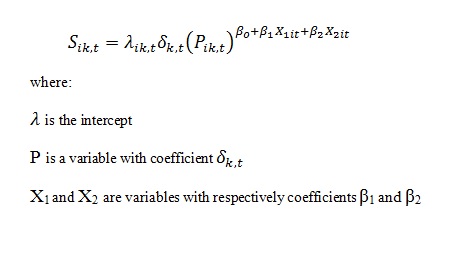

This may seem naive, but it looks like there are 5 parameters to estimate, with three independent variables and one dependent variable. Additionally, it appears, based on the subscripting, that this is a time series (indexing on t). If you can assume independence (not likely), then PROC NLIN will enable you to fit the equation. Something like:

proc nlin data=a;

parms lambda= delta= beta_0= beta_1= beta_2=;/* Provide starting values for each of the parameters */;

exponent=beta_0 + beta_1*X1 + beta_2*X2;

s = lambda * delta * P ** exponent;

output out=b predicted=yp;

run;

See if this works. It does require multiple observations, probably at least 40, to get a decent fit. Notice also that no matter what you do, lambda and delta will be completely confounded--only their product can be fit, unless there is some other constraint on one or the other.

Steve Denham

.jpg")