- Home

- /

- Analytics

- /

- Forecasting

- /

- Re: Dynamic Regression in Forecast Studio

- RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello,

I am trying to fit a dynamic regression model in forecast studio. I have one independent variable. I try to add a model throgh the subset (factored) ARIMA group and i create the transfer function. I also want to model the error term as an AR process. How can i do that? I don;t see any dialogue box like the error model options in custom model in TSFS.

Thanks in advance,

Andreas

Accepted Solutions

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello Andreas -

The TSFS dialog for custom models allows you to build "regression models with time series errors" which are also called transfer function models.

The Error Model Options you specify are actually the p (AR) and q (MA) specifications you would enter in Forecast Studios ARIMA dialog (similar for P and Q in the seasonal ARIMA case).

For example, specifying the following settings in the custom models dialog:

can be replicated in Forecast Studio like this:

Hope this helps.

Thanks,

Udo

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello -

As you probably already figured out, there are 2 dialogs related to ARIMA(X) in SAS Forecast Studio - between them you can do everything that TSFS can do (when it comes to ARIMAX) and you even have access to more features.

When you create an Autoregressive Integrated Moving Average (ARIMA) model, you can specify the autoregressive and moving average polynomials of an ARIMA model. You can also include events and independent variables in the model. When creating a Subset (factored) ARIMA model, you can specify a general ARIMA model. You can specify the autoregressive and moving average polynomials of arbitrary complexity. You can also specify a general differencing order. The Subset ARIMA Model dialog box is similar to the ARIMA Model dialog box, except that it uses a more general specification of the ARIMA options.

For more information about the ARIMA model and the Subset (factored) ARIMA model, see the HPFARIMASPEC procedure in the SAS High-Performance Forecasting: User's Guide.

Thanks,

Udo

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello Udo,

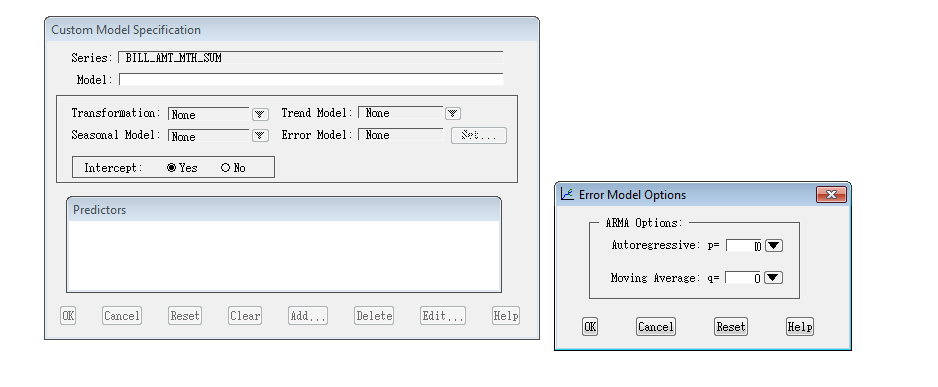

Thank you very much for your answer. In the attatched screenshot i have the dialogue box of TSFS for a custom model specification. When i want to fit the error term of my model as an ARMA process i use the error model dialogue box and i get the small window where i can determine the AR and MA terms of the error term. Can i do this in Forecast Studio? I have tried to create models using the ARIMA and the factor (subset) ARIMA dialogue boxes but i don't see such an option. Is there an option to model the error term as an ARMA process? Where is it?

Thanks in advance,

Andreas

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello Andreas -

The TSFS dialog for custom models allows you to build "regression models with time series errors" which are also called transfer function models.

The Error Model Options you specify are actually the p (AR) and q (MA) specifications you would enter in Forecast Studios ARIMA dialog (similar for P and Q in the seasonal ARIMA case).

For example, specifying the following settings in the custom models dialog:

can be replicated in Forecast Studio like this:

Hope this helps.

Thanks,

Udo

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Hello Udo,

Would it be possible to schedule a demo with you on SAS Forecast Studio? I got few questions. Mainly, can Studio run various models using several independent variables and arriving at best fit model automatically?

Thanks

Ania

- Mark as New

- Bookmark

- Subscribe

- Mute

- RSS Feed

- Permalink

- Report Inappropriate Content

Ania -

Please contact me directly by dropping me an email and we can discuss your request offline.

https://communities.sas.com/people/udo%40sas

Thanks,

Udo

.jpg")

Catch up on SAS Innovate 2026

Nearly 200 sessions are now available on demand in the Innovate Hub.

Watch Now →- Live Webinar: Unlocking Value With Managed Cloud Services | 16-Jun-2026

- Ask the Expert: Can Agents Reduce Planning Friction in CPG Supply Chains? | 16-Jun-2026

- Ask the Expert: Mit KI zur Höchstleistung: SAS Studio Copilot in Aktion! | 25-Jun-2026

- Ask the Expert: Get Meaningful Results With New Features in SAS Customer Intelligence 360 | 25-Jun-2026

- Ask the Expert: Modern, offen, skalierbar: Datenarchitektur mit SAS®Viya | 09-Jul-2026

- MinnSUG 2026 Annual SAS Conference | 22-Jul-2026

-

5 replies

-

01-11-2013 07:43 PM

-

4096 views

-

3 likes

-

3 in conversation

-